I consider it a great honour and privilege to have been invited as the Keynote Speaker on the occasion of the Dinner to celebrate the 25th Nigerian Economic Summit here today in Abuja. The organisers told me they wanted a speaker who was an active participant at the first Summit held a little over 25 years ago and who is still active today.

When I went back to read the Report of the 1st Nigerian Economic Summit which kicked off on 18 February, 1993, my first reaction was one of humility and thanksgiving to God that I am still here 25 years later; I never realised that so many out of that very first batch of Summiteers had since passed on. May their gentle souls rest in perfect peace.

My second reaction however was one of disappointment that some of the exact same economic issues and problems that plagued Nigeria then are still being debated here 25 years later. I am not claiming that we have not achieved phenomenal progress in certain areas such as telecommunications, commercial and investment banking, Pension reform and other service sector pursuits such as Information Technology, Music, Film, Art and Fashion.

The harsh reality is that whatever gains Nigeria achieved in income per capita over the course of the last two decades are slowly being wiped out, as falling annual per capita incomes have become the norm in every single year since 2015. Macroeconomists measure broad aggregates and the numbers do not lie. The investment and GDP statistics used here were obtained with the assistance of Dr Yemi Kale, who heads the National Bureau of Statistics.

Advertisement

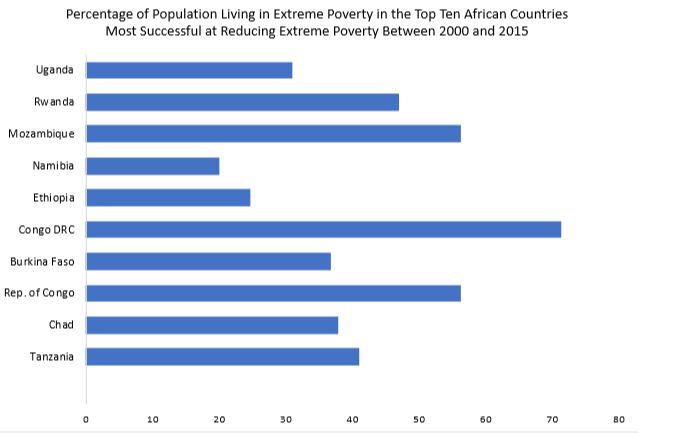

In a nutshell, falling living standards appear to have come to stay in Nigeria and so hoardes of Nigerians continue to join the ranks of the extremely poor year after year, at a time when several African countries are successfully lifting more and more of their own people out of poverty. World Bank data confirms that the African countries who have been most successful (Top ten) at reducing extreme poverty over the course of a 15-year period spanning Year 2000 to 2015 are Tanzania, Chad, Republic of Congo, Burkina Faso, Congo DRC, Ethiopia, Namibia, Mozambique, Rwanda & Uganda (See slide 1 below).

When the earlier Summits were being held in the 1990s, some of the most popular comparisons by presenters were those between Nigeria and Malaysia, Indonesia and various other Asian tigers. Today, we can clearly benefit from case studies on poverty reduction emanating from Africa’s top ten. The same can be said for education, healthcare and infrastructure where Nigeria does not feature in Africa’s top ten in terms of rapid positive change.

Advertisement

Indeed, Nigeria now leads the world in two appalling statistics: 1) the largest number of school age children out of primary school (10.5m); and 2) total number of persons living in extreme poverty (90m approx.). It was not so in 1993.

There is a frightening and ominous link between these two sets of statistics because children who are ill-equipped in terms of basic primary education are likely to be the most difficult to integrate into a 21st Century economy. Many of them were born into poverty and will remain in poverty unless we do something urgently to rescue them. Even more worrying are the regional disparities that show up when socioeconomic data is disaggregated. For instance, the WAEC May/June 2019 WASSCE results show that 9 out of the top 10 States with the best results are from the South East and South-South zones – Lagos State is the only top 10 entrant from outside these two zones. Conversely, of the bottom 8 States on this same Exam results chart, 5 are from the North West, whilst 3 are from the North East zone (See slide 2 below).

In the 1990s, rapid economic growth eluded many Sub-Saharan African economies. In 2018, the average GDP growth rate for Sub-Saharan African economies was 2.4%, but if you exclude the two largest economies (Nigeria and South Africa), who are both laggards, then the GDP growth rate for the rest of Sub-Saharan Africa immediately leaps up to 5%. We therefore no longer need to go to Asia to learn lessons about rapid growth. We only need to look to Ivory Coast and Senegal in West Africa which grew at 7.40% and 7.0% respectively or to Ethiopia and Rwanda in East Africa, which grew by 8.50% and 7.20% respectively in 2018.

Advertisement

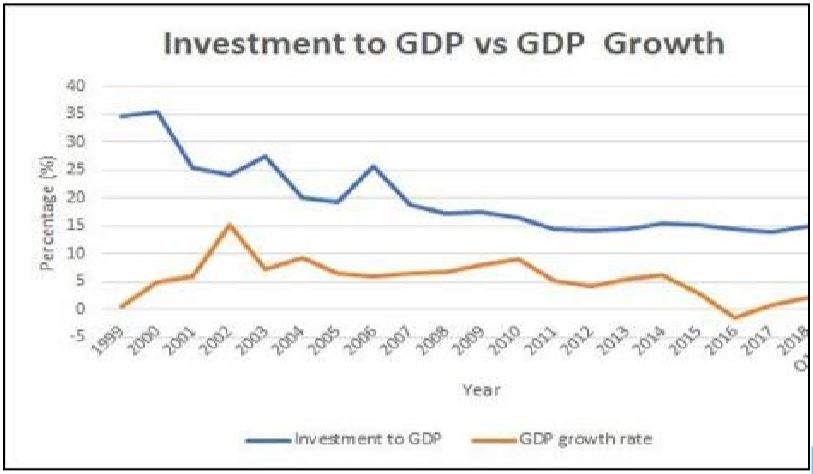

The fore-runner of GDP growth is the Investment/GDP ratio. If there are little or no investments today, then there will be little or no growth in a couple of years’ time. The double-digit growth of 2002 came on the back of the very high Investment/GDP ratio of 35% recorded in year 2000, which was the first full year following the restoration of democracy. Thereafter, the long term trend for Nigeria’s Investment/GDP ratio has been a near-continuous downward slide. By 2012, the Investment to GDP ratio had slid all the way to below 15% and so GDP growth rates were bound to fall sharply after 2013 (see Slide 3 below).

As GDP growth rates fizzled out in 2015 and 2016, the Central Bank of Nigeria (CBN) compounded the situation by embarking on forex policies which caused investors to both take fright and take flight at the same time. The inevitable outcome was an economic recession. It was only after CBN succumbed to pressure in early 2017 to allow a Nafex exchange rate, where all business units and individuals could buy and sell forex freely at a market determined exchange rate of N360/$1 approx., that supply bottlenecks slowly disappeared, and the economy limped out of a recession. The Nigerian economy is however still largely stagnant and so anaemic GDP growth rates which fall below the approximate 3% population growth rate are not cause for celebration. With high inflation rates in the 11% range, which CBN appears to have accepted as being the norm, investors now fear stagflation. Compare and contrast this with Ivory Coast and Senegal which held inflation below 2% and grew GDP in excess of 7% in 2018.

Before going into prescriptions, it is important to update this audience about the current structure of the Nigerian economy, which is significantly different from what prevailed in 1993 in 5 important areas:

Advertisement

1) Over 50% of our GDP now comes from the Service Sector. CBN appeared to have forgotten this in 2016 when directing banks to allocate 60% of forex to the manufacturing sector that accounted for less than 10% of GDP. CBN also held out the false hope that denial of forex to specific sectors of the economy would somehow incentivise investors in other sectors. The reality is that draconian actions directed at one group of investors simply make other investors think “so who is next and/or what is next”? A corollary of this proposition is to point out that actions and pronouncements that increase overall Uncertainty and Risk are likely to be counter-productive, if the goal is to boost investment activity generally;

2) Inward diaspora remittances now eclipse the oil and gas sector as the number one source of forex for Nigeria. Again, CBN overlooked this while trying to force these inflows to come in at a stipulated official rate of N200/$1 at a time when the parallel market had galloped beyond N400/$1 in 2016;

Advertisement

3) Our ICT sector’s GDP contribution has since outgrown the oil and gas sector share of GDP and so it should be heralded and nurtured instead of being attacked by rogue regulators as has become fashionable;

4) The split of aggregate demand between the Private Sector and the Government Sector (all 3 tiers) is now 91.5%/8.5%. Some Nigerians still dream about FG stimulating national aggregate demand through its own expenditure activity alone. Meanwhile, FG’s total 2020 budget expenditures will translate into a paltry sum of $130 or less per Nigerian. How can that possibly transform Nigeria’s economy in a meaningful way?

Advertisement

One of the first areas of consensus in that first economic summit in 1993 was that FG expenditures alone could never transform the Nigerian economy and so by far the most impactful activity that FG could engage in was to create an enabling environment and a level playing field that would stimulate phenomenal private sector investment activity. 25 years later some of our policy makers still sound as if they missed this most basic lesson.

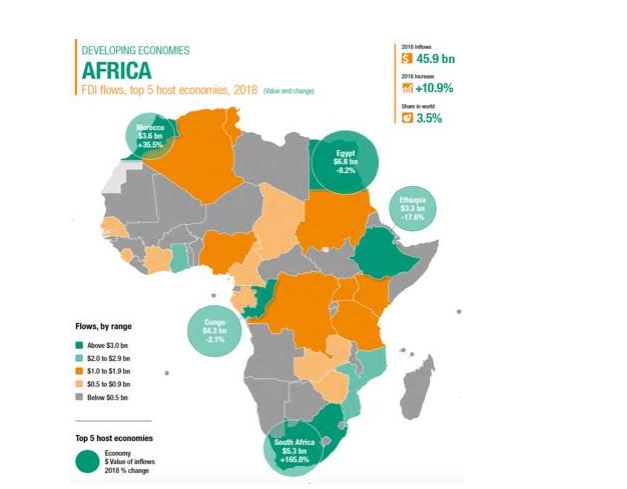

5) In 2018, Nigeria’ Foreign Direct Investment inflows slipped behind Ghana’s for the first time. In terms of FDI flows into Africa, Nigeria slipped into the second tier in 2018. The first tier is now comprised of Egypt, South Africa, Congo, Morocco, Ethiopia, Ghana and Mozambique (see slide 4 below). Indeed, Mozambique may head this chart in a few years’ time. They have provided the type of clarity which Nigeria has refused to provide to the Oil and Gas sector from the moment the Oil Minister in the previous administration produced a first draft of a myopic Petroleum Industry Bill.

Advertisement

THE WAY FORWARD

It is not too late for President Buhari’s Government and our national assembly to borrow a cue from Mozambique and learn how to enact laws that provide clarity and reduce uncertainty for investors in the oil and gas sector and other sectors too.

So, why is Nigeria unable to achieve GDP growth rates of 6% and above which are currently the norm in several Sub-Saharan Africa economies? The obvious answer is that we appear to have frightened most investors away (local and foreign) and they will not be coming back any time soon until we correct the structural dysfunction that frightened them away in the first place.

Investors appear to have concluded that the Nigerian economy is rigged against all except the very well-connected and they are right. By definition, the well-connected investors are few and so our Investment/GDP ratio is likely to remain low until we make it possible for all other investors (Nigerian and foreign) to come back and partake in the task of baking a bigger cake on the basis of a level playing field.

In Nigeria of 2019, only the well-connected can expect the following (indicated in Slide 5 as follows); 1) Security of life and property; 2) Prompt dispensation of Justice; 3) Sanctity of contracts; 4) No harassment from multiple rogue regulators; 5) Access to land via the Land Use Act; 6) Freedom from multiple illegal State and Local Government levies; 7) Provision of good roads and pipe-borne water to their doorstep; 8) Access to subsidised financing; and 9) Public sector employment opportunities.

For the youths, the less privileged and others who are not well connected, they dare not expect these 9 things. Instead, they should concentrate on avoiding being the victims of extra-judicial killings and other forms of Police (notably SARS) or Army brutality (see Slide 6 below) and if they go into a legitimate business activity, they should get ready to grapple with endless threats and harassment by FIRS, Customs, State Government Tax authorities, SARS, NAFDAC etc. The bulk of this harassment typically comes from corrupt government officials seeking to line their own pockets through extortion.

Sadly, there appears to be no oversight function and so the excesses of these rogue regulators are largely unchecked, thereby leaving no respite nor protection for their poor victims. There is no justice for the underprivileged in Nigeria and so this exacerbates Income Inequality, which is already very high, as demonstrated by our Gini Coefficient of 0.4 approx.

A new generation of Nigerians (largely youths) have been dealt a terrible hand. A Nigerian Passport gives them few options for taking flight. It is not so with investors. Many can take flight and have done so. Sadly, most utterances by important public figures give the remaining investors even more cause to worry. We need a paradigm shift away from harassing investors to one of welcoming them sincerely as well as taking actions that boost business confidence, as Morocco and Rwanda do all the time. A global race is on to win the hearts and minds of investors. Nigeria is currently losing that race badly even within Africa.

Reversing this terrible trend is a shared responsibility. A society gets the leaders that it deserves and so I do not blame this Government or past Governments. I blame the elite in general because we shy away from backing truly competent political leaders, as if we fear that we will not succeed in manipulating them or getting them to rig economic outcomes in our favour.

In the meantime, FG has lost fiscal viability because it lacks the courage to trim personnel overheads on account of a bloated headcount in the public sector. Will 98% of the population continue to suffer so that less than 2% who make up the bloated public sector can maintain their lifestyles? The same FG endorsed a largely unaffordable minimum wage and presses on with “populist” subsidies which are largely cornered by the rich. Government revenues as a percentage of GDP are exceedingly low at 6% approx and yet all that the private sector does is resist any attempts to increase indirect taxes or price products such as petrol and electricity on the basis of full cost recovery. Even the recent inevitable decision to introduce toll gates on our roads has been met by private sector resistance.

Following the launch of a new payments-enabled National ID Card it is certainly possible to quantify the annual petrol subsidy, apportion it and pay each Nigerian adult that falls below a minimum income threshold his or her share. This can be executed transparently by the same office for National Social Investment Programs that currently pays monthly handouts to a lucky few out of the 90 million extremely poor Nigerians. If FG is in the habit of being seen to grant subsidies, then we should focus less on getting stubborn people to shed a bad habit. It is far better to get them to replace a bad habit of wasted subsidies with a much better habit of direct payments to the poor via an instrument that the rich cannot corner or access.

There will be no strong economic future for Nigeria that can be built and sustained if the deal is to starve the Government of revenues, whilst blaming the 3 tiers of Government for failing to deliver on their respective mandates. The responsibility that we must share is to encourage FG to get its finances in order and attain both fiscal viability and macroeconomic stability. We must also encourage FG to level the playing field for investors and quit dangling rent-seeking and/or arbitrage opportunities such as multiple exchange rates, which remain open to abuse.

In 1993, Summiteers and CBN agreed that CBN should pursue a 5% inflation target. At that time US inflation was 3% and so the gap was only 2% p.a. Today, US inflation is 2% and yet CBN appears to be content with keeping inflation high at 10 or 11% p.a., the 9% per annum differential is much too high and is inconsistent with the declared goal of maintaining exchange rate stability. Nobody should get carried away by our short term reliance on “hot” money inflows to bolster forex reserves on the basis of distorted “carry trades”. CBN should quit expanding its mandate into other questionable areas, if it cannot meet its most basic mandate of containing inflation.

We cannot afford to approach the next 25 years by repeating the errors of the last 25 years. The shared responsibility includes getting the elite to become less insular or less sycophantic and to learn to speak truth to power. The recently appointed Economic Policy Advisory team is a step in the right direction by FG. Their job will be made a lot easier if this Summit can help establish an elite consensus on the unfinished business that is still holding us back from building and sustaining a strong economic future for Nigeria.

I thank you for your attention.

ACKNOWLEDGEMENT

I would also like to acknowledge the contributions of Ms. Edirin Akemu and Ms. Eloho Omame, CEO of Endeavor Nigeria, in helping to compile data and preparing accompanying charts and tables.

Being the keynote Address at 25th Nigerian Economic Summit Dinner, Abuja, on October 7, 2019,

Twitter: @AtedoPeterside.

Views expressed by contributors are strictly personal and not of TheCable.